Designing for Top-Tier Credit

From Insight to Concept

During my rotation at TM Studio, Ally’s internal innovation and ideation lab — I co-led and participated in a multi-day design thinking workshop focused on reimagining Ally’s credit card product.

The goal: design a top-of-wallet credit card for prime and super-prime consumers (680+ credit score) that could compete in an ultra-competitive market by going beyond standard rewards programs.

I operated at the intersection of researcher and facilitator, helping shape the questions we asked, how we listened, and how we turned raw consumer insight into testable concepts.

〰️

Tools: Miro, UserTesting, Figma, Adobe Creative Suite, Pen and Paper

Role: UX Designer, Researcher, & Co-Facilitator

Responsibilities: Customer Interviews, competitive analysis, design thinking workshops, concept testing

Note: All visuals and prototypes were recreated by me in 2026

Research Foundation

Before a single idea was generated, we grounded the session in real consumer data. My role included synthesizing survey findings and in-depth interview insights into actionable design direction.

METHODS USED

In-Depth Interviews

Competitive Analysis

Behavioral Segmentation

Concept Testing

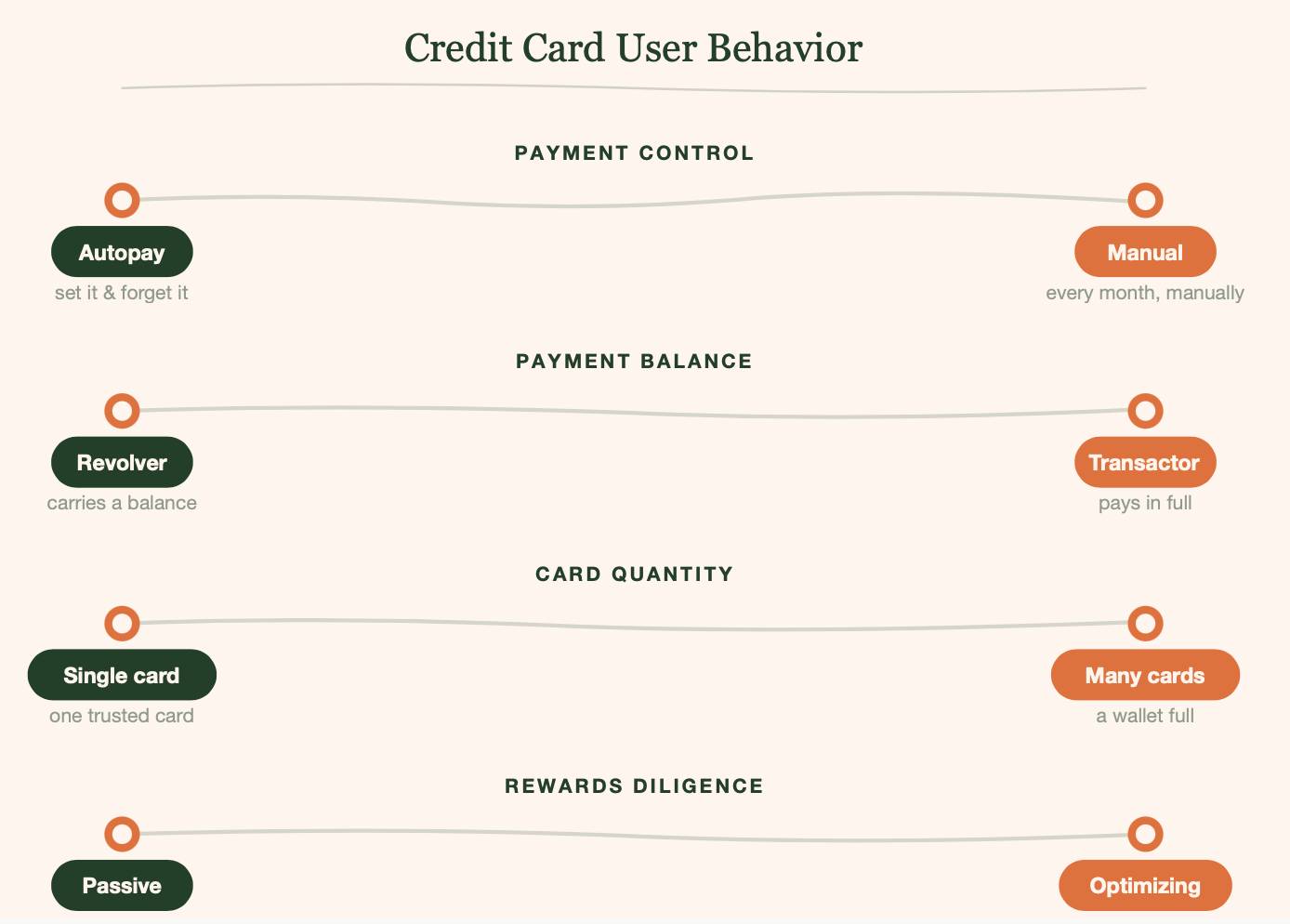

Consumer interviews revealed that prime cardholders are not a monolithic group — they vary widely in how they think about credit, what they value, and how they engage with rewards.

01

Cash is King

63% of consumers prefer cash back. Travel is a distant second. But within cash back preferences, how people want to earn and redeem varies significantly.

02

Security > Rewards

61% rank security higher than cash back (48%) or earning rewards (47%). For many, the shift to credit cards began during the pandemic — and trust has become a threshold expectation, not a differentiator.

03

Control is Non-Negotiable

60% of prime customers prefer manual payment control. Autopay felt like a loss of agency. This pattern held especially true for high-credit-score customers who were already highly engaged with their finances.

04

Rewards Drive Acquisition, Not Loyalty

Most people open cards for rewards but stay for other reasons. Gaming the system for sign-up bonuses is common. Long-term engagement requires something more meaningful than points.

Behavioral Segmentation Framework

To make sense of the diversity in our consumer data, we applied four behavioral scales that mapped how prime cardholders actually think and act — not just what they say they want.

From Research to “How Might We”

One of my core contributions was helping translate messy, qualitative consumer data into structured design challenges. We distilled everything we heard into two “How Might We” statements — each targeting a distinct opportunity space.

Provide Value

HMW Design a credit card that provides value to consumers outside of traditional rewards and sign-up incentive programs?

Research driver: Consumers felt that standard rewards programs had become commoditized. The real pain point wasn’t the size of the reward — it was the feeling that the card wasn’t working for their actual life.

Be Integrated

HMW Design a credit card that seamlessly integrates within the Ally ecosystem and provides additional value to Ally customers?

Research driver: Existing Ally customers expressed a desire for their financial products to feel connected. The card was an opportunity to reward loyalty across the whole relationship, not just spending.

Ideation & Concept Development

With our research grounding in place, we moved into structured ideation across three rounds. I co-facilitated the session while actively contributing as a member of Team Three — which required me to hold both the macro view of the room and the micro view of developing strong, defensible ideas.

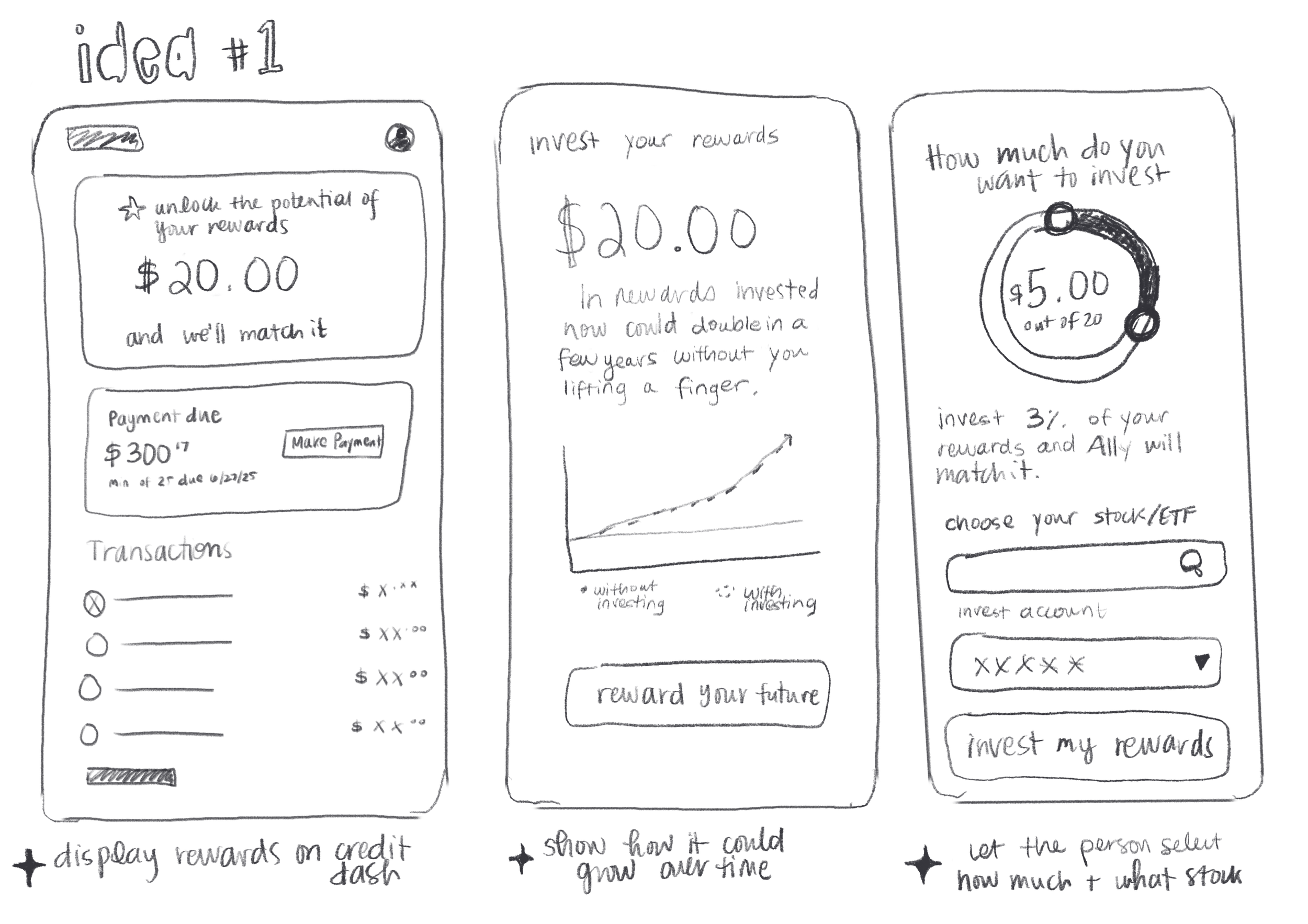

Round 1 — Designing for Value

HMW Provide value outside of traditional rewards programs.

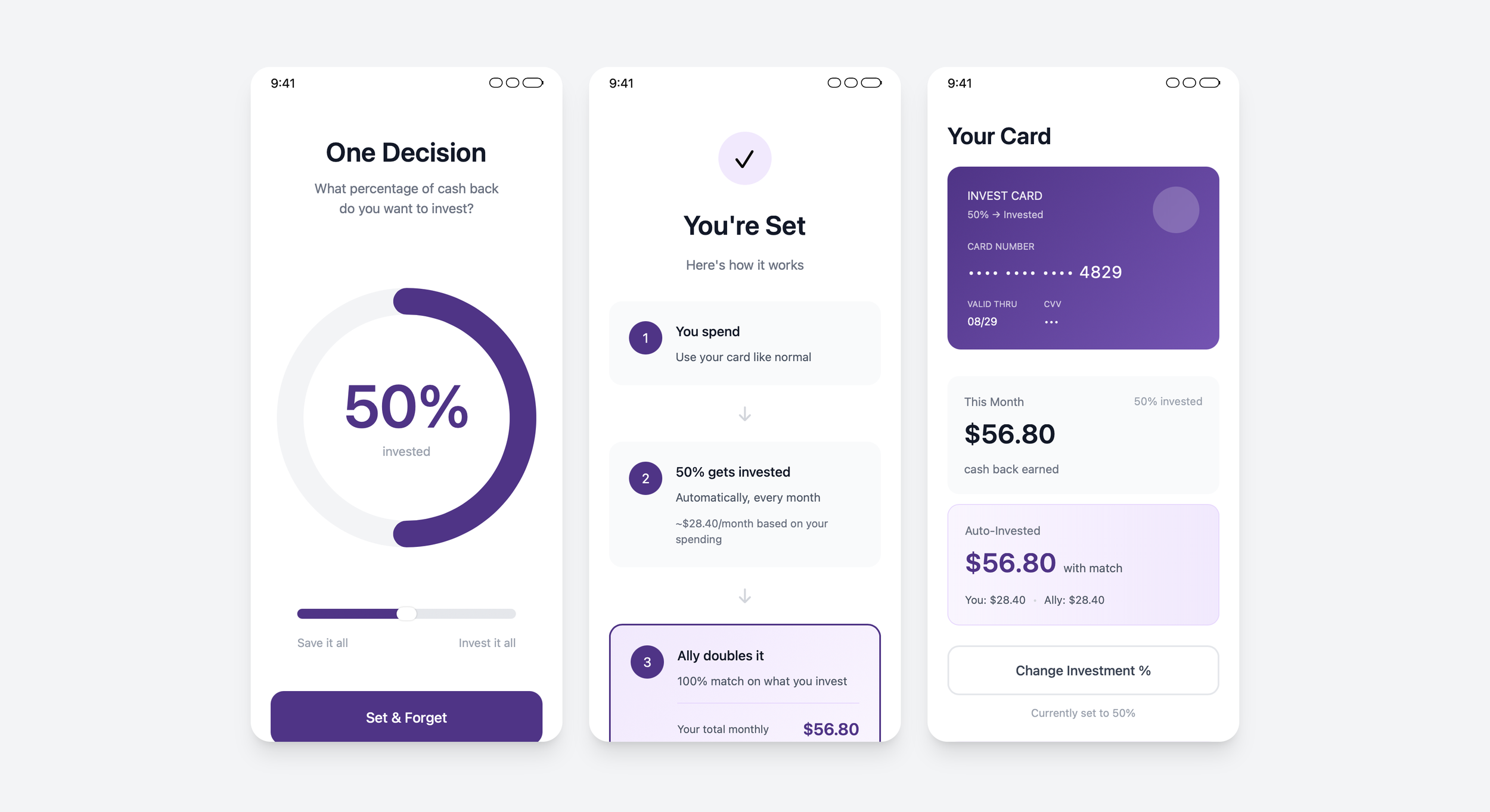

Team Three’s concept centered on a card that lets cardholders direct a portion of their cash back into an Ally investment account — with Ally matching it.

The idea reframed the reward conversation entirely: instead of points that expire or rotate, the card could move you forward financially.

Synthesis & Concept Testing

After three rounds of ideation, my team moved into rapid prototyping and concept testing — taking our strongest ideas from broad brainstorm to testable value propositions.

How We Evaluated Concepts

Ran concepts through multiple design critiques, iterating based on feedback

Tested value propositions for clarity, differentiation, and resonance with target consumer profiles

Pushed back on ideas that were creative but would not survive operationalization or regulatory constraints

Emerging Themes

What Changed Through Iteration:

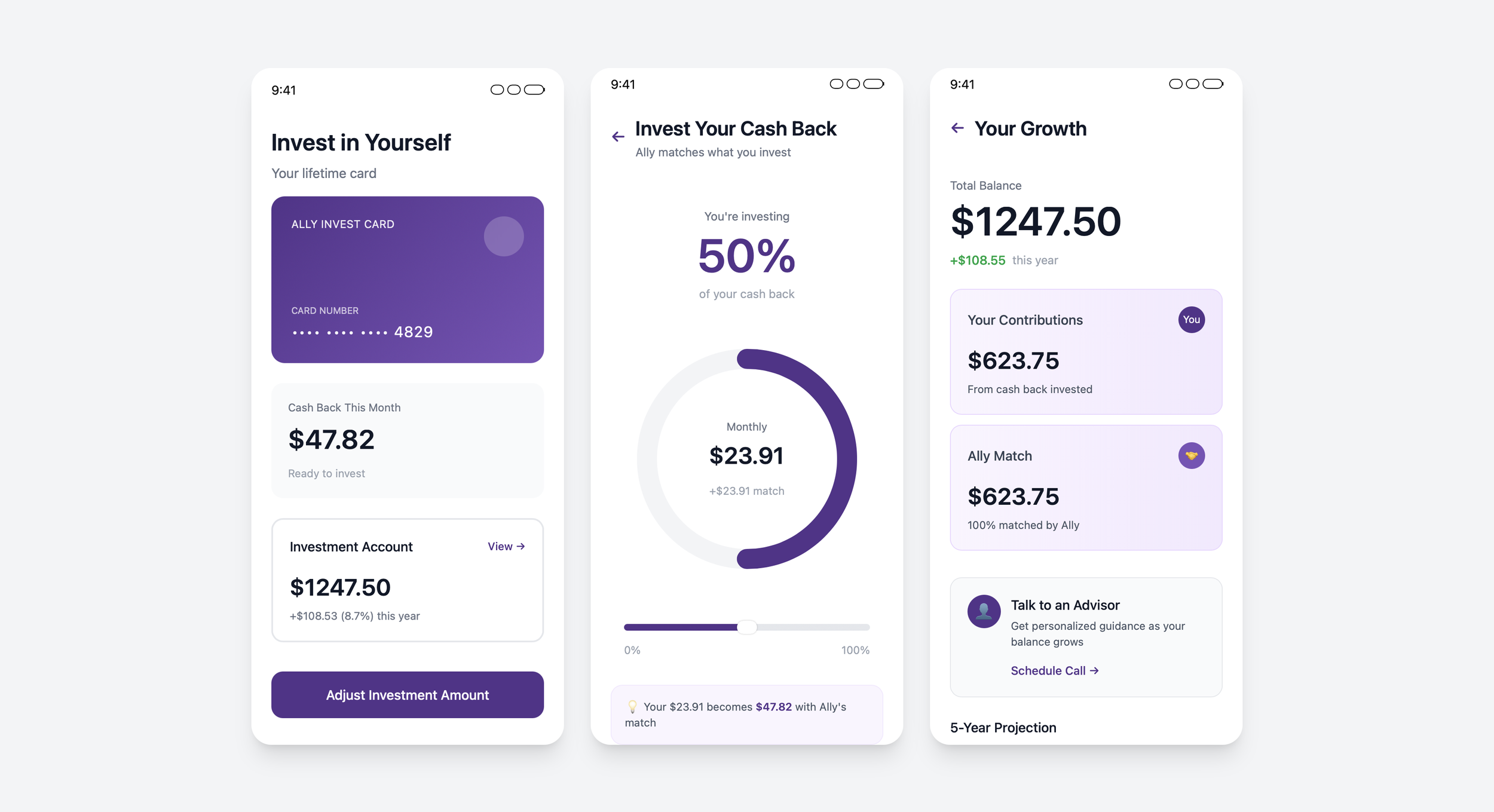

Our initial investment-matching concept was too complex — it required consumers to make too many decisions upfront.

Through critique, we simplified: instead of configuring a financial plan, users just decide what percentage of cash back to invest. One dial. Ally handles the rest. The simpler version tested stronger and felt more true to Ally’s brand voice of making finance feel achievable.

Themes that held across teams

-

🤝 Build deep, long-lasting relationships

Consumers want a card that grows with them, not one that chases them.

-

✨ Offer choice, control, and joy

Agency over how rewards work is more valuable than the reward itself.

-

🍃 Simplify with a "get more, stress less" approach

Every feature that adds complexity is a feature that won’t get used.

Invest In Yourself

〰️

Invest In Yourself 〰️

Outcome & Impact

Executive Presentation

Prototypes and research findings from this session were presented in bi-weekly stakeholder demos and culminated in a final pitch to the CEO and President of Consumer & Commercial Banking at Ally.

Successfully co-facilitated a 24-person, multi-day cross-functional design thinking session

Synthesized consumer interview data into three structured HMW design challenges that drove the entire session

Developed rapid prototypes that earned praise from the Credit Card Director through multiple rounds of critique

Contributed directly to a credit card concept grounded in behavioral consumer research and Ally’s brand strategy

Strengthened my practice in research synthesis, facilitation at scale, executive communication, and fintech product strategy

Reflection

What I valued most about this project was the discipline of listening before designing. The insights that shaped our strongest concepts came from sitting with information long enough to notice what consumers were really saying underneath their stated preferences. Interviewing real people from across the country not only made our insights diverse, but also taught me some tips and tricks on how to use credit cards that I’d never known.

Co-facilitating while actively ideating also sharpened my ability to hold the user’s perspective and the team’s creative process at the same time.